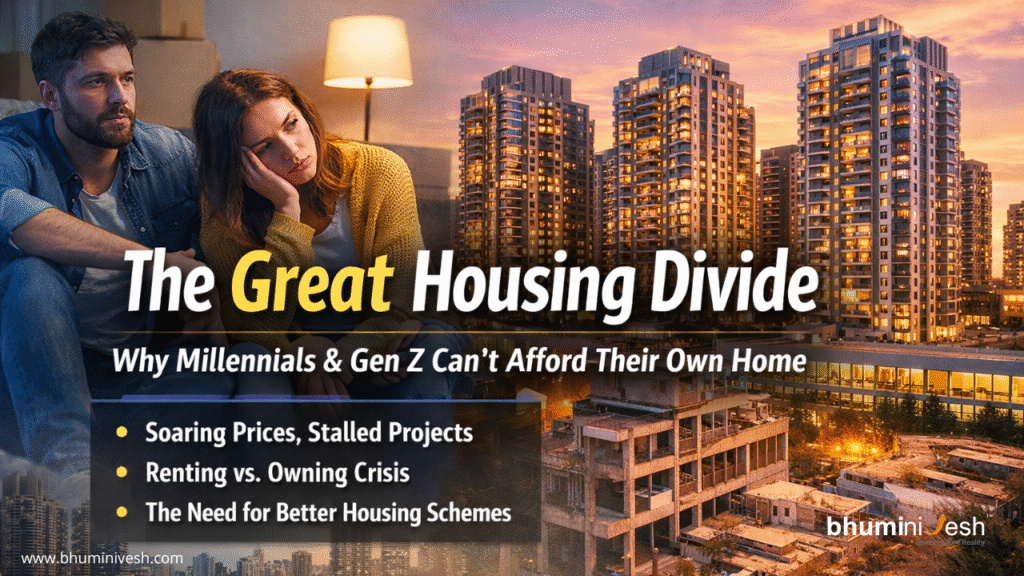

The Dream That Is Slipping Away

For previous generations, owning a home was not just a financial milestone — it was a symbol of stability, dignity, and family legacy.

Parents and grandparents who bought homes before COVID-19 or during the early pandemic years often purchased properties at prices that, in today’s market, seem almost unbelievable.

A flat that cost ₹35–45 lakh in 2019–2020 is now often priced at ₹75 lakh to ₹1 crore or more, especially in urban regions like Chandigarh, Mohali, Delhi NCR, Bengaluru, Pune, and Hyderabad.

For Millennials and Gen Z, this surge has created a brutal reality:

homeownership is moving out of reach.

Instead of buying, most young professionals are now forced into long-term renting.

And this raises a critical question:

If projects are selling out, who exactly is buying them?

Because clearly, it is not the average salaried young Indian.

The Post-COVID Real Estate Surge: What Changed?

COVID changed the housing market dramatically.

During the pandemic, interest rates were lower, developers offered aggressive discounts, and many builders were eager to liquidate inventory.

This was one of the best windows for homebuyers.

However, after 2021, the market shifted sharply.

According to a Reuters property market poll, home prices in India have more than doubled over the last decade, and are expected to continue rising. Prices were projected to rise 6.3% in 2025 and another 7% in 2026, while rents are also increasing faster than inflation.

That means the same salaried class whose income may have grown by 20–30% over five years is facing housing prices that have surged by 70–100%.

This mismatch is the heart of India’s new housing crisis.

Salary Growth vs Property Price Growth: The Broken Equation

Let’s look at reality.

A young professional earning ₹8–12 lakh per annum in cities like Mohali, Chandigarh, Gurugram, Pune, or Bengaluru may be able to safely afford an EMI of around ₹30,000–₹45,000 per month.

That typically supports a home loan of ₹35–50 lakh, depending on tenure and rates.

But the homes being launched are increasingly priced far above this range.

- 2 BHK in decent urban sectors: ₹70–90 lakh

- Premium 3 BHK: ₹1–1.5 crore

- Villas / independent floors: ₹1.5 crore+

Even homes in the ₹50 lakh–₹1 crore segment saw declining affordability and supply, while premium homes above ₹1 crore now dominate sales.

This means:

income growth has not kept pace with real estate inflation.

And this is why many millennials are delaying homeownership until their late 30s or even 40s.

Reuters notes that the qualifying age to buy a home has shifted from 30–40 years to nearly 45 years.

That is a massive structural change.

If Projects Are Sold Out, Who Is Buying Them?

This is perhaps the biggest question troubling young buyers.

They see “SOLD OUT” banners everywhere.

Luxury towers are launched and seemingly booked in weeks.

But if ordinary salaried youth cannot afford them, who is buying?

The answer lies in market polarisation.

1. High-Net-Worth Individuals (HNIs)

Luxury housing demand has surged from wealthy buyers, business owners, NRIs, and investors.

Homes above ₹1 crore accounted for nearly 50% of annual sales in 2025.

2. Investors and Wealth Preservation Buyers

Real estate is increasingly being treated as a store of wealth.

For affluent investors, property acts as:

- inflation hedge

- rental asset

- long-term capital appreciation

3. NRI Investment Capital

Many projects in metro and tier-1 growth corridors are heavily purchased by NRIs.

4. Institutional / bulk investors

Some inventory is absorbed by large investment groups.

This leaves first-time homebuyers competing in a market designed around capital rather than shelter.

The Death of Affordable Housing Supply

One of the most alarming trends is that affordable housing itself is shrinking.

According to Knight Frank data, affordable housing demand fell 17% year-on-year, while new launches declined 28%.

Affordable housing under ₹40–50 lakh now forms only a small share of supply.

In many cities, this segment is disappearing.

Reports show homes priced below ₹1 crore dropped sharply across major cities.

This is because developers are chasing higher margins.

Luxury housing gives better profitability than affordable units.

So builders are naturally moving toward premium projects.

For Gen Z and millennials, this creates a supply vacuum.

Why Renting Is Becoming the Default Lifestyle

This is why renting is now replacing ownership.

Young professionals are making a rational financial decision.

Instead of taking on a ₹60,000 EMI for 25 years, many prefer paying ₹20,000–₹30,000 rent.

This offers:

- flexibility

- mobility

- lower financial stress

- career freedom

- better location access

But there is also an emotional cost.

For Indian families, homeownership is deeply linked to identity and social security.

Renting often feels temporary.

This creates anxiety, especially among millennials who grew up seeing parents buy homes in their early 30s.

The Psychological Impact on Millennials and Gen Z

This crisis is not only financial.

It is emotional.

Many young people now feel that no matter how hard they work, the dream keeps moving further away.

This affects:

- marriage planning

- family expansion

- long-term wealth creation

- mental peace

- lifestyle choices

The idea of owning a spacious 3 BHK with a balcony, study room, and family space now feels unrealistic.

Instead, many settle for smaller rented apartments.

The dream has shifted from “my home” to “a manageable rent.”

Fraud, Delayed Projects, and Stalled Construction

Another major issue is trust.

Many young buyers hesitate because several projects are either delayed, stuck in legal disputes, or halted by government authorities.

This has happened due to:

- land title disputes

- environmental clearance issues

- builder financial mismanagement

- RERA violations

- regulatory stoppages

This further damages buyer confidence.

When a young person saves for years and invests in an under-construction property that gets stuck, the financial damage can be devastating.

This is one reason many prefer ready-to-move rentals instead.

Why PMAY and Government Schemes Need Urgent Revision

This is where policy intervention becomes essential.

Pradhan Mantri Awas Yojana has delivered over 122 lakh houses under PMAY-Urban till November 2025, according to the Economic Survey.

This is commendable.

However, the scheme now needs a major revision for the urban middle class and first-time salaried buyers.

Because today’s challenge is no longer only EWS/LIG housing.

The new challenge is:

the squeezed middle-income generation

Young professionals earning ₹8–20 lakh annually are falling through the cracks.

They earn too much for some subsidies.

But too little for market prices.

This is the real affordability gap.

What the Government Should Do Next

Here are policy measures that can truly help millennials and Gen Z:

1. Revise PMAY income slabs

Current eligibility should be expanded for urban salaried professionals.

2. Interest subsidy for first-time buyers under 40

Lower effective loan rates for first-home purchases.

3. Incentives for sub-₹75 lakh housing

Builders should get tax and FSI incentives for affordable launches.

4. Rental-to-own housing model

A structured system where rent contributes toward eventual ownership.

5. Faster approvals for affordable projects

Reduce regulatory delays and compliance costs.

6. Stronger anti-fraud enforcement

RERA and local authorities must ensure strict completion accountability.

Where Is This Leading?

If this continues unchecked, India may witness a generational wealth divide.

Older generations who bought property before COVID will continue to benefit from asset appreciation.

Younger generations may remain renters for decades.

This creates:

- wealth inequality

- delayed family formation

- lower asset ownership

- social dissatisfaction

The housing market cannot remain sustainable if the working middle class is permanently excluded.

Final Thoughts: A Dream That Must Not Die

Homeownership should not become a privilege reserved only for investors and the wealthy.

A country grows strongest when its working generation can build roots.

Millennials and Gen Z are not asking for luxury.

They are asking for dignity.

A safe, spacious, affordable home.

That dream must not be lost.

India needs a new housing policy vision that recognises this generation’s reality.

Because when an entire generation stops dreaming of owning a home, it is not just a market issue.

It is a social issue.

It is an economic issue.

And it is a policy issue.